Are you confused while determining value of supply in case foreign Currency Exchange ?

RULE: 32 Determination of value in respect of certain supplies.-

- Notwithstanding anything contained in the provisions of this Chapter, the value in respect of supplies specified below shall, at the option of the supplier, be determined in the manner provided here in after.

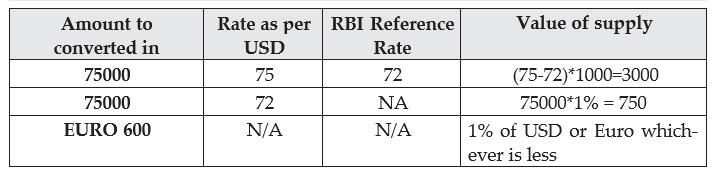

- The value of supply of services in relation to the purchase or sale of foreign currency, including money changing, shall be determined by the supplier of services in the following manner, namely:-

- for a currency, when exchanged from, or to, Indian Rupees, the value shall be equal to the difference in the buying rate or the selling rate, as the case may be, and the Reserve Bank of India reference rate for that currency at that time, multiplied by the total units of currency:

- Provided that in case where the Reserve Bank of India reference rate for a currency is not available, the value shall be one per of the gross amount of Indian Rupees provided or received by the person changing the money:

- Provided further that in case where neither of the currencies exchanged is Indian Rupees, the value shall be equal to one per cent. of the lesser of the two amounts the person changing the money would have received by converting any of the two currencies into Indian Rupee on that day at the reference rate provided by the Reserve Bank of India.

EXAMPLE

Provided also that a person supplying the services may exercise the option to ascertain the value in terms of clause (b)(i.e. Composition Scheme) for a financial year and such option shall not be withdrawn during the remaining part of that financial year.

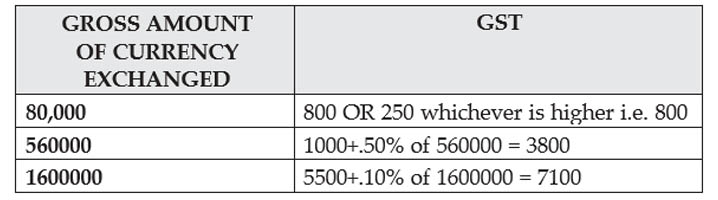

at the option of the supplier of services, the value in relation to the supply of foreign currency, including money changing, shall be deemed to be-

- one per cent. of the gross amount of currency exchanged for an amount up to one lakh rupees, subject to a minimum amount of two hundred and fifty rupees;

- one thousand rupees and half of a per of the gross amount of currency exchanged for an amount exceeding one lakh rupees and up to ten lakh rupees; and

- five thousand and five hundred rupees and one tenth of a per of the gross amount of currency exchanged for an amount exceeding ten lakh rupees, subject to a maximum amount of sixty thousand rupees.