Case Study

Atlas Publishing limited is a company engaged in publishing of Journals, books, reference works etc. in the field of social sciences, sciences, humanities, technology and medicine.

The following is the Trial Balance of the company for the month of September’2019:

| Sr. No. | Income | Amount |

| 1. | Commission on books | 5,00,000 |

| 2. | Commission on Journals | 2,50,000 |

| 3. | Sale of published books – Domestic (50% Intra-State sales) | 60,00,000 |

| 4. | Sale of published Journals – Domestic (75% Intra-State sales) | 28,00,000 |

| 5. | Export of Books | 94,00,000 |

| 6. | Export of Journals | 80,00,000 |

| 7. | Export of E-books (OIDAR) | 72,00,000 |

| 8. | Domestic sale of E-books & E-Journals (OIDAR) | 68,00,000 |

| 9. | Sale of Scrap (Intra-state) | 2,00,000 |

| 10. | Interest on Bank Deposits (Intra-state) | 12,00,000 |

| 11. | Profit on sale of shares (Intra-state) | 3,50,000 |

| 12. | Profit on sale of motor vehicles (Intra-state) | 1,80,000 |

| 13. | Bad Debts recovered (Intra-state) | 5,50,000 |

| Total | 4,34,30,000 | |

Details of Expenses along with ITC:

| Sr. No. | Expense | Amount | ITC |

| 1. | Printing (20% C&S) | 1,10,00,000 | 5,50,000 |

| 2. | Editing & Publishing (40% C&S) | 80,00,000 | 14,40,000 |

| 3. | Royalty on Books & Journals (50% C&S) | 15,00,000 | – |

| 4. | Health Insurance of Employees (C&S) | 5,00,000 | 90,000 |

| 5. | Advertising & Recruitment Expenses (25% (C&S)) | 8,00,000 | 1,44,000 |

| 6. | Generator running expense (C&S) | 2,00,000 | 36,000 |

| 7. | Import of OIDAR | 90,00,000 | 16,20,000 |

| 8. | Festival Expense (C&S) | 2,00,000 | 36,000 |

| 9. | Stock Insurance (C&S) | 7,00,000 | 1,26,000 |

| 10. | Vehicle Insurance (C&S) | 3,00,000 | 54,000 |

| 11. | Audit Fee (C&S) | 2,50,000 | 45,000 |

| 12. | Legal Fee (25% of the fee pertains to CA and the remaining to advocate) (C&S) | 3,00,000 | – |

| 13. | Salary | 55,00,000 | – |

| 14. | Shipping & Courier Expense (C&S) | 12,00,000 | 2,16,000 |

| 15. | Freight – Local (C&S) | 4,00,000 | 20,000 |

| 16. | Rent (C&S) | 27,00,000 | 4,86,000 |

| 17. | Security Services (C&S) | 3,00,000 | 54,000 |

| 18. | Repair & Maintenance (C&S) | 5,00,000 | 90,000 |

| Total | 3,61,50,000 | 50,07,000 | |

Other Information:

- Commission on Books & Journals is in relation to books & journals sold in India and Exported. The Bifurcation of the same is provided below:

| Particulars | Amount |

| Commission on Books – Export | 2,00,000 |

| Commission on Books – Domestic (Inter-state) | 3,00,000 |

| Commission on Journals – Export | 1,00,000 |

| Commission on Journals – Domestic (Inter-state) | 1,50,000 |

- The Exports are undertaken without payment of tax with LUT. Refund of ITC for quarter ending June’19 needs to be filed in relation to exports without payment of tax. The information regarding same is provided below:

| Particulars for quarter ending June’19 | Amount |

| ITC: | |

| CGST | 32,00,000 |

| SGST | 32,00,000 |

| IGST | 70,00,000 |

| Export Turnover (before credit notes) | 6,50,00,000 |

| Exempt Turnover | 4,80,00,000 |

| Taxable Turnover | 3,00,00,000 |

| Credit Notes in relation to Export Turnover | 30,00,000 |

Out of the above ITC, the following ITC pertains to supplies which are totally exempt:

CGST: 10,00,000

SGST: 10,00,000

IGST: 22,00,000

3. In relation to Export of E-books & E-journals, the sales are made to educational institutions and other than educational institutions also. The bifurcation of the same is provided below:

| Particulars | Amount |

| E-books to Educational Institutions (25% Intra-state) | 20,00,000 |

| E-books to others (60% Intra-state) | 18,00,000 |

| E-Journals to Educational Institutions (45% Intra-state) | 14,00,000 |

| E-Journals to others (75% Intra-state) | 16,00,000 |

| Total | 68,00,000 |

4. Sale of scrap involves sale of laptops amounting to Rs. 80,000.

Sale of office furniture amounting to Rs. 70,000.

Sale of mobile phones amounting to Rs. 50,000.

5. For the purpose of Rule 42:

Exempt Turnover: 3,00,00,000

Taxable Turnover: 4,80,00,000

Export Turnover: 2,20,00,000

6. Profit on sale of motor vehicles: (Intra-state)

| Particular | Amount |

| Purchase value (no ITC availed on this purchase) | 18,00,000 |

| Depreciation till date under IT Act | 9,50,000 |

| Depreciation till date as per company act | 7,50,000 |

| Sales value | 11,30,000 |

Questions:

- Comment on the applicability of GST on Publishing of Books.

- Calculate the amount of tax payable on inter-state and intra state sales.

- Calculate the amount of Refund for the quarter ending June’19.

- Comment on the treatment of sale of Motor Vehicle.

- What is the place of supply in case of OIDAR Services?

- Classify the expense under Reverse charge along with rate of tax. Also, determine the amount of tax payable under reverse charge.

- Calculate the amount of eligible ITC.

- Calculate the amount of Net tax payable.

Answers:

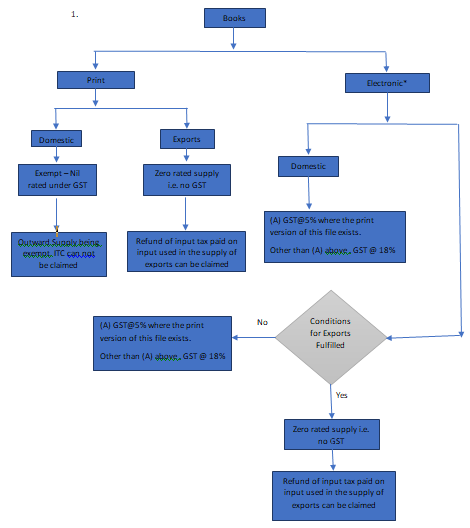

1.

*Points to be noted in case of Electronic Mode:

| Nature of Services | Description | Taxability |

| Online Educational Journals & Periodicals provided to Educational Institutions. | Supply of Online Educational Journals & Periodicals to Educational Institutions. | Exempt w.e.f. 25.01.2018, earlier taxable. |

| OIDAR other than the one above | Supply of Online Journals & Periodicals (other than educational) to Educational Institutions.Supply of Online books (other than Educational Journals & Periodicals) to Educational Institutions.

Supply of Online Educational Books/Journals & Periodicals to other persons. |

Taxable |

(Refer Note 1)

2. Calculation of tax payable on intra-state and inter-state supplies:

| Sr. No. | Income | Tax Amount | Intra State | Inter State |

| 1. | Commission on books | 5,00,000 | – | – |

| 2. | Commission on Journals | 2,50,000 | – | – |

| 3. | Sale of published books – Domestic | 60,00,000 | – | – |

| 4. | Sale of published Journals – Domestic | 28,00,000 | – | – |

| 5. | Export of Books | 94,00,000 | – | – |

| 6. | Export of Journals | 80,00,000 | – | – |

| 7. | Export of E-books (OIDAR) | 72,00,000 | – | – |

| 8. | Domestic sale of E-books & E-Journals (OIDAR) | |||

| -E-books to Educational Institutions (25% Intra-state) | 20,00,000 | – | – | |

| -E-books to others (60% Intra-state) | 18,00,000 | 1,94,400 | 1,29,600 | |

| -E-Journals to Educational Institutions (45% Intra-state) | 14,00,000 | – | – | |

| -E-Journals to others (75% Intra-state) | 16,00,000 | 2,16,000 | 72,000 | |

| 9. | Sale of Scrap (Intra-state) | |||

| -Laptop | 80,000 | 14,400 | – | |

| -Office Furniture (Wooden) | 70,000 | 8,400 | – | |

| -Mobile Phones | 50,000 | 9,000 | – | |

| 10. | Interest on Bank Deposits (Intra-state) | 12,00,000 | – | – |

| 11. | Profit on sale of shares (Intra-state) | 3,50,000 | ||

| 12. | Profit on sale of motor vehicles (Intra-state) Margin on sale (refer point 4 of solution) | 2,80,000 | 50,400 | – |

| 13. | Bad Debts recovered (Intra-state) | 5,50,000 | – | – |

| Total | 4,34,30,000 | 4,63,800 | 2,01,600 | |

3. Calculation of refund for the quarter ending June’19:

Refund Amount (Rule 89(4)) = Turnover of Zero-rated Supply of Goods and Services/Adjusted Total Turnover*Net Input Tax Credit

Turnover of Zero-rated Supply of Goods and Services = 6,50,00,000 – 30,00,000

= 6,20,00,000

Adjusted Total turnover = 6,20,00,000 + 3,00,00,000

= 9,20,00,000

Net Input Tax Credit = (32,00,000 + 32,00,000 + 70,00,000) – (10,00,000 + 10,00,000 + 22,00,000)

= 92,00,000

Refund = 6,20,00,000/9,20,00,000*92,00,000

= 62,00,000*

(* Assuming that the balances in Electronic credit ledger as on the date of filing such refund and at the end of the period to which such refund pertains exceeds the amount of refund calculated as per Rule 89(4) above)

(*Zero-rated supply of service (Rule 89) is the aggregate of the payments received during the relevant period for zero-rated supply of services and zero-rated supply of services where supply has been completed for which payment had been received in advance in any period prior to the relevant period reduced by advances received for zero-rated supply of services for which the supply of services has not been completed during the relevant period)

(Refer Note 2)

4. Notification No. 8/2018- Central Tax (Rate) dated 25th January’2018 was issued which talked about the taxability under GST in case of sale of old vehicle.

According to the above-mentioned notification:

- GST shall be applicable @ 18% (or 12% as the case may be) on the margin of the supplier.

- Where the margin of the supplier is negative, it shall be ignored.

How to calculate Margin of the Supplier:

- In case of a registered person where depreciation under section 32 of Income Tax Act’1961 has been claimed, the margin of supplier shall be the difference between the consideration received for such supply and the depreciated value of such vehicle on the date of supply.

Margin of Supplier = Selling Price (-) Depreciated Value of Vehicle

- In any other case, the margin of the supplier shall be the difference between the selling price and the purchase price of the vehicle.

Margin of Supplier = Selling Price (-) Purchase Price of Vehicle

The said notification will not be applicable where the input tax credit has been availed by the supplier od such old motor vehicle under GST Act or under CENVAT Credit rules or VAT.

Keeping in mind the above notification, lets calculate the taxability or otherwise of the sale of motor vehicle:

| Particulars | Amount |

| WDV as on date as per IT Act (18,00,000-9,50,000) | 8,50,000 |

| Sale Value | 11,30,000 |

| Margin (11,30,000-8,50,000) | 2,80,000 |

| GST @ 18% (CGST=25,200/- & SGST=25,200/-) | 50,400 |

5. According to Section 13 sub-section 12 of the IGST Act’2017, the place of supply of online information and database access or retrieval services shall be the location of the recipient of services.

Explanation. ––For the purposes of this sub-section, person receiving such services shall be deemed to be located in the taxable territory, if any two of the following noncontradictory conditions are satisfied, namely:

(a) the location of address presented by the recipient of services through internet is in the taxable territory;

(b) the credit card or debit card or store value card or charge card or smart card or any other card by which the recipient of services settles payment has been issued in the taxable territory;

(c) the billing address of the recipient of services is in the taxable territory;

(d) the internet protocol address of the device used by the recipient of services is in the taxable territory;

(e) the bank of the recipient of services in which the account used for payment is maintained is in the taxable territory;

(f) the country code of the subscriber identity module card used by the recipient of services is of taxable territory;

(g) the location of the fixed land line through which the service is received by the recipient is in the taxable territory.

6. Expenses under Reverse Charge

| Sr. No. | Expenses | Amount | Tax Rate | IGST | CGST | SGST |

| 1. | Royalty on Books & Journals | 15,00,000 | 12% | 90,000 | 45,000 | 45,000 |

| 2. | Import of OIDAR | 90,00,000 | 18% | 16,20,000 | – | – |

| 3. | Legal Fee | 3,00,000 | 18% | – | 20,250 | 20,250 |

| Tax Payable under Reverse Charge | 1,08,00,000 | 17,10,000 | 65,250 | 65,250 |

(Refer Note 3)

7. Calculation of eligible ITC

| Sr. No. | Expense | Amount | ITC | IGST | CGST | SGST | Eligibility |

| 1. | Printing (20% C&S) | 1,10,00,000 | 5,50,000 | 4,40,000 | 55,000 | 55,000 | Eligible (C2) |

| 2. | Editing & Publishing (40% C&S) | 80,00,000 | 14,40,000 | 8,64,000 | 2,88,000 | 2,88,000 | Eligible (C2) |

| 3. | Royalty on Books & Journals (50% C&S) | 15,00,000 | 1,80,000 | 90,000 | 45,000 | 45,000 | Eligible (C2) |

| 4. | Health Insurance of Employees (C&S) | 5,00,000 | 90,000 | – | 45,000 | 45,000 | Blocked (T3) |

| 5. | Advertising & Recruitment Expenses (25% (C&S)) | 8,00,000 | 1,44,000 | 1,08,000 | 18,000 | 18,000 | Eligible (C2) |

| 6. | Generator running expense (C&S) | 2,00,000 | 36,000 | – | 18,000 | 18,000 | Eligible (C2) |

| 7. | Import of OIDAR | 90,00,000 | 16,20,000 | 16,20,000 | – | – | Eligible (C2) |

| 8. | Festival Expense (C&S) | 2,00,000 | 36,000 | – | 18,000 | 18,000 | Blocked (T3) |

| 9. | Stock Insurance (C&S) | 7,00,000 | 1,26,000 | – | 63,000 | 63,000 | Eligible (C2) |

| 10. | Vehicle Insurance (C&S) | 3,00,000 | 54,000 | – | 27,000 | 27,000 | Blocked (T3) |

| 11. | Audit Fee (C&S) | 2,50,000 | 45,000 | – | 22,500 | 22,500 | Eligible (C2) |

| 12. | Legal Fee (25% of the fee pertains to CA and the remaining to advocate) (C&S) | 3,00,000 | 54,000 | – | 27,000 | 27,000 | Eligible (C2) |

| 13. | Salary | 55,00,000 | – | ||||

| 14. | Shipping & Courier Expense (C&S) | 12,00,000 | 2,16,000 | – | 1,08,000 | 1,08,000 | Eligible (C2) |

| 15. | Freight – Local (C&S) | 4,00,000 | 20,000 | – | 10,000 | 10,000 | Ineligible (T2) |

| 16. | Rent (C&S) | 27,00,000 | 4,86,000 | – | 2,43,000 | 2,43,000 | Eligible (C2) |

| 17. | Security Services (C&S) | 3,00,000 | 54,000 | – | 27,000 | 27,000 | Eligible (C2) |

| 18. | Repair & Maintenance (C&S) | 5,00,000 | 90,000 | – | 45,000 | 45,000 | Eligible (C2) |

| Total | 3,61,50,000 | 52,41,000 | |||||

Application of Rule 42:

| Particulars | Amount |

| Total Turnover | 10,00,00,000 |

| Exempt Turnover | 3,00,00,000 |

| Common ITC (C2)-Total | 50,41,000 |

| IGST | 31,22,000 |

| CGST | 9,59,500 |

| SGST | 9,59,500 |

| Blocked ITC (T3) | 1,80,000 |

| Ineligible ITC (T2) | 20,000 |

| ITC not available (5041000*30000000/100000000) | 15,12,300 |

| ITC to be availed (50,41,000-15,12,300) | 35,28,700 |

| CGST | 6,71,650 |

| SGST | 6,71,650 |

| IGST | 21,85,400 |

(Refer Note 4)

8. Net Tax Payable

| Particulars | IGST | CGST | SGST |

| Tax Payable | |||

| Intra State Inter State Under RCM | 2,01,600 17,10,000 | 2,31,900 – 65,250 | 2,31,900 – 65,250 |

| ITC Availed Forward & RCM | 21,85,400 | 6,71,650 | 6,71,650 |

| Net Tax Payable RCM (in cash) Forward Charge (through ITC) | 17,10,000 2,01,600 | 65,250 2,31,900 | 65,250 2,31,900 |

Notes:

Note 1: Explanation to Answer 1

- The Central Government exempts the supply of goods of description as specified below (N.No. 02/2017 (CT) dt. 28/06/2017):

- Printed books, including Braille books.

- The Central Government exempts the supply of services of description as specified below (N.No. 12/2017 (CT)dt. 28/06/2017):

- Services by way of:

(b)(v) supply of online educational journals or periodicals.

- The Central Government specifies the rate of tax on supply of services of description as specified below (N.No. 11/2017 (CT Rate) dt. 28/06/2017):

- Supply consisting only of e-book shall be taxable @ 5% (IGST) (2.5%- CGST & SGST each)

For the purposes of this notification, “e-books” means an electronic version of a printed book.

Note 2: explanation to Answer 3

As per Rule 89(4) of CGST Rules 2017, In the case of zero-rated supply of goods or services or both without payment of tax under bond or letter of undertaking in accordance with the provisions of sub-section (3) of section 16 of the Integrated Goods and Services Tax Act, 2017 (13 of 2017), refund of input tax credit shall be granted as per the following formula –

Refund Amount = (Turnover of zero-rated supply of goods + Turnover of zero-rated supply of services) x Net ITC ÷Adjusted Total Turnover

Where,

“Net ITC” means input tax credit availed on inputs and input services during the relevant period other than the input tax credit availed for which refund is claimed under sub-rules (4A) or (4B) or both.

“Turnover of zero-rated supply of goods” means the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking, other than the turnover of supplies in respect of which refund is claimed under sub-rules (4A) or (4B) or both

“Turnover of zero-rated supply of services” means the value of zero-rated supply of services made without payment of tax under bond or letter of undertaking,

“Adjusted Total Turnover‖ means the sum total of the value of-

(a) the turnover in a State or a Union territory, as defined under clause (112) of section 2, excluding the turnover of services; and

(b) the turnover of zero-rated supply of services determined in terms of clause (D) above and non-zero-rated supply of services,

excluding-

(i) the value of exempt supplies other than zero-rated supplies; and

(ii) the turnover of supplies in respect of which refund is claimed under sub-rule (4A) or sub- rule (4B) or both, if any, during the relevant period.

Note 3: Explanation to Answer 6

Notification No. 13/2017-CENTRAL TAX (RATE), DATED 28-6-2017, enlists certain services wherein the recipient of service is liable to pay tax under reverse charge:

| Category of Service | Supplier of Service | Recipient of Service |

| Services provided by an individual advocate including a senior advocate or firm of advocates by way of legal services, directly or indirectly | An individual advocate including a senior advocate or firm of advocates. | Any business entity located in the taxable territory |

| Supply of services by an author by way of transfer or permitting the use or enjoyment of a copyright covered under clause (a) of sub-section (1) of section 13 of the Copyright Act, 1957 relating to original literary works to a publisher | Author | Publisher located in the taxable territory |

Note 4: Explanation to Answer 7

Section 17 of CGST Act, 2017, read with rule 42 of CGST Rules 2017, provides the apportionment of Input Tax Credit. According to this the input tax credit in respect of inputs or input services, being partly used for the purposes of business and partly for other purposes, or partly used for effecting taxable supplies including zero rated supplies and partly for effecting exempt supplies, shall be attributed to the purposes of business or for effecting taxable supplies in the following manner, discussed below—

- the total input tax involved on inputs and input services in a tax period, be denoted as ‘T’

- the amount of input tax, out of ‘T’, attributable to inputs and input services intended to be used exclusively for the purposes other than business, be denoted as ‘T1‘

- the amount of input tax, out of ‘T’, attributable to inputs and input services intended to be used exclusively for effecting exempt supplies, be denoted as ‘T2‘

- the amount of input tax, out of ‘T’, in respect of inputs and input services on which credit is not available under sub-section (5) of section 17, be denoted as ‘T3‘

- the amount of input tax credit credited to the electronic credit ledger of registered person, be denoted as ‘C1‘ and calculated as—

C1 = T- (T1+T2+T3)

- the amount of input tax credit attributable to inputs and input services intended to be used exclusively for effecting supplies other than exempted but including zero rated supplies, be denoted as ‘T4‘

- ‘T1‘, ‘T2‘, ‘T3‘ and ‘T4‘ shall be determined and declared by the registered person at the invoice level

- input tax credit left after attribution of input tax credit used exclusively for effecting supplies other than exempted but including zero rated supplies shall be called common credit, be denoted as ‘C2‘ and calculated as—

C2 = C1 – T4

- the amount of input tax credit attributable towards exempt supplies, be denoted as ‘D1‘ and calculated as—

D1= (E÷F) × C2

where,

‘E’ is the aggregate value of exempt supplies during the tax period, and

‘F’ is the total turnover in the State of the registered person during the tax period:

Provided further that where the registered person does not have any turnover during the said tax period or the aforesaid information is not available, the value of ‘E/F’ shall be calculated by taking values of ‘E’ and ‘F’ of the last tax period for which the details of such turnover are available, previous to the month during which the said value of ‘E/F’ is to be calculated.

- the amount of credit attributable to non-business purposes if common inputs and input services are used partly for business and partly for non-business purposes, be denoted as ‘D2‘, and shall be equal to 5% of C2 and

- the remainder of the common credit shall be the eligible input tax credit attributed to the purposes of business and for effecting supplies other than exempted supplies but including zero rated supplies and shall be denoted as ‘C3‘, where,—

C3 = C2 – (D1+D2);

- the amount ‘C3’, ‘D1’ and ‘D2’ shall be computed separately for input tax credit of central tax, State tax, Union territory tax and integrated tax

the amount equal to aggregate of ‘D1‘ and ‘D2‘ shall be reversed by the registered person.